Facilities Management as we know it was borne out of the recessions of the 1970s and 80s. The challenges forced upon organisations by the difficult economic circumstances of those years created the need for a different kind of workplace and a new breed of workplace manager. That need was met by the emergence of modern facilities management which built upon the basic accommodation function of previous generations.

That first decade shaped an approach centred on innovation in workplace design and a shift from a focus on compliance towards more service oriented FM operations. The last twenty years of relative economic security has allowed that initiative to develop into a recognised profession supported by a significant industry but what will the catastrophic economic meltdown of 2009 mean for FM over the next decade?

THE INDUSTRY

The outsourcing industry enables a significant part of the facilities management footprint and has flourished in the dynamic economic market of the last twenty years. Consolidation and acquisition activity has become prevalent and indications are that the supply and procurement of consolidated FM services will continue to grow in the near term, as pricing pressures remain keen. Meanwhile new entrants have continued to enter the market from all sectors in pursuit of a safe haven in the economic storm.

It seems probable that this polarisation of the FM outsourcing market will continue in the decade to come. By 2020 a distinct “premier league” of major players is likely to tower above the wider market commanding a significant portion of public sector and FTSE 350 accounts along with the fast growing international sector. Meanwhile a host of smaller FM operators will support the SME market and will increasingly focus on specialist services in niche markets where the margins are highest and where technical expertise is valued above low cost core service provision.

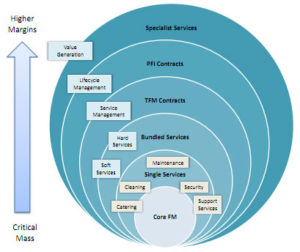

Core facilities management services like catering, cleaning, guarding and building maintenance are liable to become increasingly commoditised as operating methodologies become standardised and the pricing power of the market diminishes. The premium margins commanded by “solutions providers” will be restricted to those services which are closest to the client organisations own core operations and thus valued in the eye of the purchaser.

Larger organisations where more sophisticated procurement enables bulk purchasing of multiple services across diverse estates are beginning to remove such premium services from their bundled FM contracts and this seems likely to continue. Large scale management models provide a highly efficient model for the integration and co-ordination of multiple services but cannot compare with specialist providers for excellence in technical service delivery.

Once the benefits from risk transfer and economies of scale have been captured and systemised, the dilution of service focus will become exposed. Client organisations will prioritise certain service lines above others where the impact on their own strategy may be put at risk. This will lead to unbundling or even in-sourcing to a resurgent in house FM operation.

THE PROFESSION

One of the principal drivers behind the outsourcing of facilities management, as opposed to facilities service delivery, has been the scarcity of FM expertise. Every recruiter in the sector knows that good FMs are hard to find. After more than 30 years of activity the profession is still relatively unknown to the general populace and most FMs still enter the field as some kind of second career rather than as a vocational choice.

FM specific qualifications have been slow to develop and the take-up by practitioners has been even slower. With FM vacancies continually exceeding the number of experienced managers seeking work there is little to motivate busy FMs to enrol and few employers can afford to allow their overstretched FMs time out to study. The challenge for the next ten years is to use the qualification career path now established to attract and develop a generation of new recruits direct from full time education or from within the frontline of service delivery operatives.

By 2020 it is to be hoped that this strategy will have paid off and that the skill shortage which has beset the profession for so long may have lessened in severity. However, formal education alone will not be enough to make Facilities Management an attractive career option. The profile and reputation of FM itself must move away from its association with sanitary engineering and outsourcing and embrace a more positive agenda if it is to fulfil its potential.

The poor image of FM is the biggest barrier to the widespread adoption of the function as a fully developed profession. Most people responsible for the management of workplace services still do not call themselves facility managers if they have even heard the term. Only a small percentage of people who carry out what could be defined as an FM role currently belong to a professional association and with no single organisation dominating the field there has been little impetus behind the professionalisation of the discipline.

The next ten years should see this problem resolved as one of the current organisations finally achieves pre-eminence. The demand by practitioners for Chartered status and the Royal Institute of Chartered Surveyors (RICS) new Associate route to Chartered Facilities Management Surveyor designation may give them the advantage here although the Chartered Management Institute (CMI), Chartered Institute of Building (CIOB) and British Institute of Facilities Management (BIFM) are among the other bodies competing for that space.

THE PRACTICE

Like any service discipline, the practice of facilities management has always been driven by the needs of its customers and the environmental factors impacting upon them. The oil crisis of the 1970s, property supply and demand problems in the 1980s and the boom times of the 1990s all influenced the innovations that FM developed during those years. The same will be true of the period up to 2010.

The impact of a global economic meltdown on a scale not seen for 70 years will leave its mark on business and society in many ways. The adoption of lean management techniques, creative problem solving and collaborative working practices is likely to be a significant feature of both industry and profession as they address waste and inefficiency in the economy and the FM supply chain.

For facilities management to lead this war on waste and to lend its considerable weight behind the recovery agenda, collaboration must be a vital element of the FM manifesto. The industry and the profession that it supports must unite behind a common purpose and articulate the message of service integration and workplace efficiency in a cohesive and compelling manner.

The Latham report of 1994 acted as an emergency siren for the construction industry triggering a wave of change in a sector that had been dominated by inefficiencies, adversarial contracting and a disjointed supply chain. Commissioned to examine this by both government and industry, Sir Michael Latham identified the potential for up to 30% savings in the total cost of construction projects through greater collaboration, smarter procurement and the elimination of waste. Over the next ten years the FM sector has the opportunity to unite behind a similar agenda in a collaborative campaign against inefficiency, over manning and double handling.

THE VISION

By grasping the opportunities offered by the need for economic recovery along with other serious challenges like climate change and shifting demographics, facilities management can make significant progress in the ten years ahead. By 2020 the FM industry will have reached new levels of maturity, the facilities profession will have made important progress and the practice of FM will have been elevated in the economic hierarchy. How big these step changes are will depend on the commitment and vision of the current leadership and the appetite for change of FM practitioners everywhere.